401k Maximizer & ETF Maximizer

The 401k Maximizer by 401k Maximizer, Inc. was developed exclusively for the American Airlines Super Saver 401K Plan.

The 401k Maximizer was developed so that every employee at American Airlines can have a powerful, easy tool to manage their 401K dollars. The 401k Maximizer solves 401K fund selection decisions immediately. Every employee should be taking advantage of the tax deferred power of our 401K Plan, but most of us just don't know how to maximize our returns and limit our risk when the market turns down. The 401k Maximizer will show you how to grow your 401K account and avoid losses that threaten your retirement. 401k Maximizer gives busy employees the bottom line on what to do with their 401K account, so they can build a secure retirement and not worry about their money.

How many times have we all witnessed colleagues of ours working weekends, holidays or all night shifts just to pick up a few extra dollars in after tax money. And yet those same folks won't take 5 minutes a month to manage their 401k accounts which will have a far greater impact on their financial future than those few extra hours every month on the job. Remember, that our 401k dollars are all tax deferred and our salaries are taxable. So do yourself, and your family, a favor and make it a habit to spend the 5 minutes every month it takes to re-allocate those 401k dollars.

During the last week of every month we will show you which funds to own, and how much exposure Conservative, Moderate and Aggressive investors should have in the market, the following month. Then every day we analyze the risk/reward potential of the overall market and let you know if any significant changes occur which would warrant you to reduce or increase your 401K market exposure and how. Stay safely on track toward reaching a secure retirement. This service will show you when to avoid high-risk times in the markets and times when the odds for solid growth are in your favor. Then it's just a matter of following the fund recommendations.

The power of this approach is so effective that you will soon be telling other employees you work with about the difference it has made in your 401K plan since you signed up. Because every American Airlines employee deserves the peace of mind of a secure retirement we want each of you to maximize your 401K investment returns. A secure retirement is one of the greatest gifts you can give yourself. Don't hesitate, subscribe now and start turning your tax deferred retirement dollars into the retirement security 401k plans were meant to be.

Top Down Investing

At 401k Maximizer,Inc. we approach the market from a top down perspective. First we evaluate overall market conditions to evaluate the risks in the market which will determine the level of market exposure Conservative, Moderate and Aggressive risk investors want their portfolios to have in the next month.

To demonstrate the power of analyzing overall market conditions before investing our hard earned 401K dollars let's compare the returns you would have realized using a simple 50 day moving average of the NASDAQ and S&P 500 indexes to evaluate whether it's safer in the market our out of the market, in the safety of cash (or in our case the credit union), during the period from 1972 to 1993.

For the S&P 500, buy and hold from 1972 to 1993 would have returned 349.96%, compared to 533.21% using a 50 day moving average to get in and out of the market. With the NASDAQ, buy and hold would have returned 760.74%, compared to 6,016% with timing.

If you had started out with $10,000, buy and hold would have increased that amount to $44,996 on the NYSE and $86,074 on the NASDAQ. Using a simple 50day moving average would have increased those numbers to $63,321 on the NYSE and $611,686 on the NASDAQ.

If you had bought and held the Dow Industrials from 1970 to 1994, you would have gained 472.62%. If you missed the 75 best days, you would have lost 51.56% of your money. But if you had missed the 75 worst days, you would have made 5,187%!!

We were so fascinated by this at 401k Maximizer, Inc. that we took it all the way back to 1928 and found that if you had purchased the Dow Jones industrial average index with $10,000 in 1928 and held it until the end of 2002, that $10,000 would have to grow to $330,807. If you had missed the 10 best months in the market since 1928, we're only talking about 10 months here in close to a 900 month period, then that $10,000 would have only grown to $47,387. But if you had missed the 10 worst months in the market since 1928 that initial $10,000 value would have grown to $3,713,036!! So it definitely pays to be in the safety of cash during the worst periods in the market, as most of you know who rode the market down during 2000 through the winter of 2002. The easy conclusion of all of this testing is that the key to making big profits over the long term is to avoid the market altogether during big sell offs.

Market Analysis

So how do we determine whether it's safe or not to dip our toes into the market at any given time? Well after many years of testing; back testing, forward testing, and just all around crazy testing we have found that relying upon any one indicator, like a moving average, or even two moving averages, is a very dangerous way to approach the market. Why? Because even the best indicators breakdown at times and don't work!!

So when you have your hard earned dollars on the line it's wiser to take a consensus of some of the best market barometers available to determine whether the wind is at your back or pushing you back. Consequently, our market analysis of both the large cap stocks as represented by the S&P 500 stocks or small cap stocks as represented by the Nasdaq Composite is a product of 7 different measurements of price direction, accumulation vs. distribution, and several measures of underlying market breadth. Each of these major signals represents a consensus vote of all of the underlying indicators which drive them. The consensus of the vote shows us the positive or negative bias of the market. Consequently, if any indicator, like a moving average, breaks down and stops performing for a period of time, its failure is masked by the consensus of the other indicators, which are still performing. We look at these indicators using weekly bars of market change to dampen out short term market noise and gain a clear picture of actual market bias.

When the consensus of all 7 underlying indicators of both the S&P 500 and the Nasdaq Composite turn negative we recommend that Conservative and Moderate risk investors reduce their market exposure. Because as the losses everyone took during the bear market show, there are times when it's just better to have money invested in the safety of cash than watch it dwindle away in any investment.

Fund Selection

So how do we select our monthly recommendations? First of all, it’s important to remember that the Super Saver fund selections producing the greatest returns will slowly change during the course of a year. This is why we want to upgrade our portfolios monthly to stay invested in the funds which have the greatest potential for gains in the following month. To select those funds, we evaluate multiple measures of each of the funds returns. This is a proprietary ranking process which considers each funds recent and historical returns. This approach is considered one of the most robust mutual fund selection techniques available.

Summary

The Advantages of using 401k Maximizer, Inc. as your guide to Super Saver fund selection:

- We start with a top down analysis of the overall market and use advanced multiple measures of underlying market breadth and strength driven by 7 different proprietary indicators all voting against each other to determine the markets bias.

- This market bias determines the level of market risk which in turn drives the level of market exposure that Aggressive, Moderate, and Conservative risk investors want to have on a month to month basis.

- We rank all of the Super Saver funds using a thoroughly tested methodology that weighs each fund’s recent and longer term returns.

To summarize, our goal is to always position ourselves for the greatest returns based upon the current market conditions with the understanding that once in a great while the greatest returns may be the safety of cash in the credit union fund.

Notes: The information and data contained herein are compiled from the J.P. Morgan web site and other sources and are believed to be reliable, but accuracy cannot be guaranteed. 401k Maximizer, Inc. disclaims any and all liability for losses that may be sustained as a result of using the data presented herein. Past performance is no assurance of future results. All investments involve risk. You should invest only after careful examination of fund prospectuses.

401k Maximizer, Inc. monitors fund performance and publishes a monthly newsletter. The goal of 401k Maximizer is to take the guess work out of the 401k choices and to help every employee manage his or her own 401k plan. 401k Maximizer is a newsletter monitoring the 401k investment alternatives available to employees of American Airlines, American Eagle and other employees of AMR Corp. American Airlines is a registered trademark of AMR Corp.

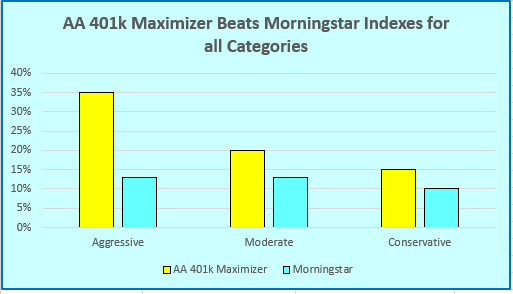

Performance

401k Maximizer has published the AA 401k Maximizer Newsletter every month since the beginning of 2006. While past performance does not guarantee future performance our record has been excellent and has provided long-term superior results.

There are several other services available to manage my American Airlines Super Saver 401k with, what makes your system better?

That's a great question. There are two main issues you want to consider when managing your 401k. The first is a method to show you when it's safe for conservative and moderate risk investors to be fully invested or with a scaled back market exposure, in the safety of the Credit Union fund, and the second is a thoroughly tested fund selection system.

We say managing your 401k because each of us should be actively upgrading our 401k holdings to the best performing funds monthly if you want to outperform the market over the long term. Buy and hold asset allocation is a recipe for underperformance whether it's with your 401k or with other dollars. Look at it this way. Money is constantly rotating on Wall Street from sector to sector and industry to industry. Normally, when the market favors a certain area like oil stocks, or biotech, or international stocks those areas will start to trend, and trend, and trend, for months on end. If the Super Saver funds you bought to hold 2 years ago don't hold the kind of stocks that are being favored by the market at the time, then they will languish month after month under performing the major indexes and occasionally even lose money when the rest of the market is going up. This is why it's critically important to constantly upgrade your Super Saver holdings to the funds which are out performing the others over the recent past in order to focus your investments in those funds which are holding the stocks that the major institutions are accumulating at the time.

Before jumping into the market though you want to analyze overall market conditions to determine whether the market currently has a positive or negative bias. The 401k Maximizer Major Market Analysis tells conservative and moderate risk investors whether it's safe to be fully invested or partially invested in the safety of the credit union as we walk forward in time.

This whole issue is so important it forms the backbone of the 401k Maximizer. At 401k Maximizer we look at 7 different measures of underlying market internals, sometimes referred to as market breadth, of both the NASDAQ and the NYSE to determine how aggressive our fund recommendations should be. These market internals gauge the strength of both the NASDAQ's and NYSE's up volume, down volume, advancing issues, declining issues, accumulation, distribution, and trend strength on a weekly basis. All of this information forms a consensus of either positive or negative market bias displayed by two simple indicators for each index. We show both of these indicators to our subscribers in every month end newsletter. The indicators then drive our recommendations about whether it's safe to be fully invested or partially invested in the safety of the Credit Union fund at the time.

The second key component of any successful method to manage our 401k funds with is a fund selection system. 401k Maximizer uses an enhanced ranking method based upon each fund’s multi-period weighted returns. This approach is considered one of the most robust mutual fund selection techniques available and has been used very successfully for years by professional money management firms specializing in mutual fund up-grading.

Which investment method is best for me? Risk vs. Reward

The Aggressive method stays 100% invested in the best ranked funds on a rolling month to month basis. This allows investors who don't like adjusting their market exposure to account for current market conditions, to stay invested in the highest ranked funds. In most market conditions, short of a bear market, the Aggressive method will probably out perform the Moderate and the Conservative risk approaches, but not by a lot, and clearly not enough so that subscribers approaching retirement, or in retirement, or subscribers who just don’t want to see their account values decrease a lot from their peak values should follow the Aggressive approach.

Conservative and Moderate risk portfolios reduce their market exposure by scaling out of the holding in the Pre-Mix fund to lower portfolio volatility when the bias of the market becomes negative.

There are several other value added features of the 401k Maximizer system that you'll want to carefully consider, including:

- Ease of Use

- Clear, user friendly, presentation

- Specific Recommendations for Conservative, Moderate and Aggressive investors

Portfolios for Conservative and Moderate risk investors that reduce your market exposure when the risk in the market increases and gets you fully invested in top ranked funds when the market bias is positive.

The 401k Maximizer uses all of the J.P. Morgan price data for each available fund. Some of the other services use an incomplete list of the funds in our Super Saver 401k system, or they use surrogate fund data to make recommendations. It is critically important to use all of the J.P. Morgan price data each month otherwise one could easily lose out on the best opportunities.

Recommendations are made before the end of the month, in order to give you time to re-allocate before the beginning of the new month.

Why spend all the time upgrading my 401k holdings every month? I feel more comfortable just buying and holding 4 or 5 good funds.

One of the golden nuggets of our 401k plan is the ability to upgrade to the best performing funds monthly without worrying about short term capital gains taxes and the commissions you would incur trying to do this through a normal low cost broker. Consider this, the commission to buy and sell a fund from a low cost broker outside of our 401k plan might run $50 to $100 per month every time you made a change. Then multiply this times holding 5-6 funds at a time and you can see how the expenses alone would kill your performance very quickly.

To see the real power of constantly upgrading to the best performing funds on a rolling month to month basis let's compare similar gains in the market with a buy and hold system versus an upgrade system. Hypothetically, we're going to make 2 investments. In our first investment we buy fund ABC at the beginning of the year and hold it for the entire year. Let’s assume our buy and hold strategy produces a return of 20% for the year, a great return! With our second investment we buy fund ABC at the beginning of the year and then sell it several months later with an 8% gain. Our model now says to buy fund DEF which we purchase and hold for a 7% gain. Next, the model says to buy fund GHI which we hold for a -2% loss. Finally, our model says to buy fund JKL which we hold to the end of the year for a 7% gain. Now by the end of the year our upgrading has produced what appears to be a similar 20% gain = +8%, +7%,-2%, +7% but in reality we made more money than buy and hold. Our buy and hold approach gained 20% but our upgrading produced a yearly gain of 21.18%!!

How did this happen? It's because when we continually upgrade to the best performing funds throughout the course of a year we are constantly leveraging our gains from the previous investment into our new investment. To make this clearer from the example above after our first gain of 8% a $100 starting value is now worth $108. So when we make the next purchase with a gain of 7% we are realizing a gain of 7% on our original $100 investment plus a gain of 7% on the $8 gain from the first investment. Remember that our account had grown to $108 before we made the second investment. And when you do that over and over and over again throughout the year you leverage your gains with the power of compounding again and again. It's that power of compounding gains over and over again that is the magic golden nugget of our Super Saver 401k. Albert Einstein referred to the power of compounding as the 8'th wonder of the world and when you see it in practice you have to agree that not only does E = M*C*C but that compounded gains are magical!

How do I use your system?

It's easy. Just subscribe and you will receive an email message around 3 - 4 days before the end of each month announcing that new recommendations are available. This message will prompt you as a subscriber to log into the 401k Maximizer web site and Sign In to view the new Recommendations and Market Analysis. 401k Maximizer is published several days before the end of every month in order to give subscribers time to re-allocate to the new recommendations before the beginning of the new month. 401k Maximizer is also published during the course of the month if any significant market changes have occurred which would warrant a re-allocation or reduction in market exposure. If you do not receive an email message towards the end of each month, you can always visit the web site and Sign In and see if they new recommendations have already been posted.

Can you explain the 90 day Re-Purchase restriction?

There have been many questions about the new 90 repurchase restriction that have been placed upon all of the funds except the Pre-Mixes. This confusion has been partially compounded by the different responses to questions about the restriction that representatives from J.P. Morgan have given about it in the past.

There are two completely different cases where and how the 90 day repurchase restriction may effect you so read closely.

The first case is for those who have purchased and held one of the funds with a 90 day repurchase restriction over 90 days ago. Let’s assume that you purchased the XYZ fund more than 90 days ago. If this is the case and you decide to sell the fund today then you can repurchase the fund again the very next day without any kind of restriction preventing you from doing so. This only applies to funds that have been purchased and held for more than 90 days.

The second case is for funds which have been purchase within the past 90 days. If you sell any fund with a repurchase restriction that you have purchased within the last 90 days, you cannot repurchase it again into you account for 90 days.

Consequently, whenever we are holding funds in our 401k account that have a 90 day repurchase restriction on them it’s important to keep track of when you purchased them, and if you have purchased the fund within the past 90 days, recognize that you cannot repurchase that fund again if you sell it for another 90 days. But if we own a fund that we purchased more than 90 days ago, recognize that this restriction is not in effect.

What do I do if the Dreyfus Premier Emerging Market fund and the T. Rowe Price Science and Technology funds are both top ranked funds in any given month?

If this happens, our recommendation is to place 10% of your money in Dreyfus Premier Emerging Market fund and 10% into the T. Rowe Price Science and Technology fund and the remaining 80% divided evenly amongst the remaining top 2 ranked funds.

Where should I designate my monthly contributions to Super Saver be deposited?

Aggressive risk investors will need to occasionally (once every couple of months) move the money from the top ranked Pre-Mix fund into the top ranked funds using the Fund to Fund Transfer feature of the web site to accomplish this transfer. But if you forget to do so, and money is left in the top ranked Pre-Mix fund for several months, this should not significantly affect your overall portfolios performance, because the performance of the top ranked pre-mix fund is generally very strong.

Changes in future allocations or Contributions (new money) must be made 3 business days prior to payday for the change to be effective with that pay check. Here are the easy steps to take care of this so it happens automatically with each paycheck.

- Log into the 401K website at (www.retireonline.com)

- Log in with your Social Security Number and personal access code.

The next page you see is labeled "My Accounts". - Click on the "Super Saver 401k Plan" link (in blue).

This brings up the "Account Balance Page". On the left side of this screen is a section with two major categories, "Account Detail" and "Account Management". - Under the "Account Management" heading is a link that says "Manage Investments". Click on it.

- On this page you will be given four major choices: View Your Investment Summary, Fund to Fund Transfer, Rebalance your account, and Change Future Investments. Select the link labeled Change Future Investments.

- This next screen will allow you to select where you want the money coming out of your paycheck to go. Scroll down to the Investment choice section and match the recommended percentages shown on page 2 of the newsletter.

- Then choose the Continue button at the bottom of the screen.

Can you please help clarify how to accomplish everything you've told me on J.P. Morgan's web site? It's a little confusing.

How do I accomplish a fund to fund transfer using the J.P. Morgan site?

- Log into the 401K website at (www.retireonline.com)

- The next page you see is labeled “My Accounts”.

- Click on the “Super Saver 401k Plan” link (in blue).

- This brings up the "Account Balance Page". On the left side of this screen is a section with two major categories, "Account Detail" and "Account Management". Under the "Account Management" heading is a link that says "Manage Investments". Click on it.

- On this page there are four links in the middle of the page labeled View Your Investment Summary, Fund to Fund Transfer, Rebalance your account, and Change Future Investments. Select the link labeled “Fund to Fund Transfer”.

- Scroll down the page and select the fund you want to sell, and then at the bottom of the page under Transfer Type select “Percentage Amount”, and in the box labeled “Amount to Transfer” fill in 100%.

- Select the “Continue” button.

- Now select the fund you are going to transfer the money from the fund you selected on the previous page into, and put 100% in the box in the column labeled “New %”.

- Select the “Continue” button.

- Then Accept.

Please note that if a transfer request is made on a business day by 2:59 PM Central Time, the transfer is processed that day and is based on the fund closing prices that day. Transfer requests received on or after 3 PM Central time are processed the following day based on the closing price of the funds on that day.

If you still have questions about your account or whether you are doing this correctly call J.P. Morgan at (1-800-345-2345) and tell them what percentages you want in each fund.

Notes: The information and data contained herein are compiled from J.P. Morgan and are believed to be reliable, but accuracy cannot be guaranteed. 401k Maximizer, Inc. disclaims any and all liability for losses that may be sustained as a result of using the data presented herein. Past performance is no assurance of future results. All investments involve risk. You should invest only after careful examination of fund prospectuses.

401k Maximizer, Inc. monitors fund performance and publishes a monthly newsletter. The goal of 401k Maximizer is to take the guess work out of the 401k choices and to help every employee manage his or her own 401k plan. 401k Maximizer is a newsletter monitoring the 401k investment alternatives available to employees of American Airlines, American Eagle and other employees of AMR Corp. American Airlines is a registered trademark of AMR Corp.

Below are example recommendations for a prior time period --- for 1/26/04 for your AA Super Saver 401k.

These recommendations are provided by 401k Maximizer.

This analysis last updated on: 01/26/04